Energy Risk Forecaster: Why have wholesale energy costs fallen this winter?

For the most part of 2018, wholesale energy prices saw a steep upward curve, compounding the impact of rising non-commodity costs on UK business and leading to warnings of a ‘double blow’ for consumer energy bills.

However, over the final quarter of last year and through to early 2019, wholesale costs have settled. Why is this the case? And how will this affect businesses going forward?

Background – What caused wholesale costs to increase in 2018?

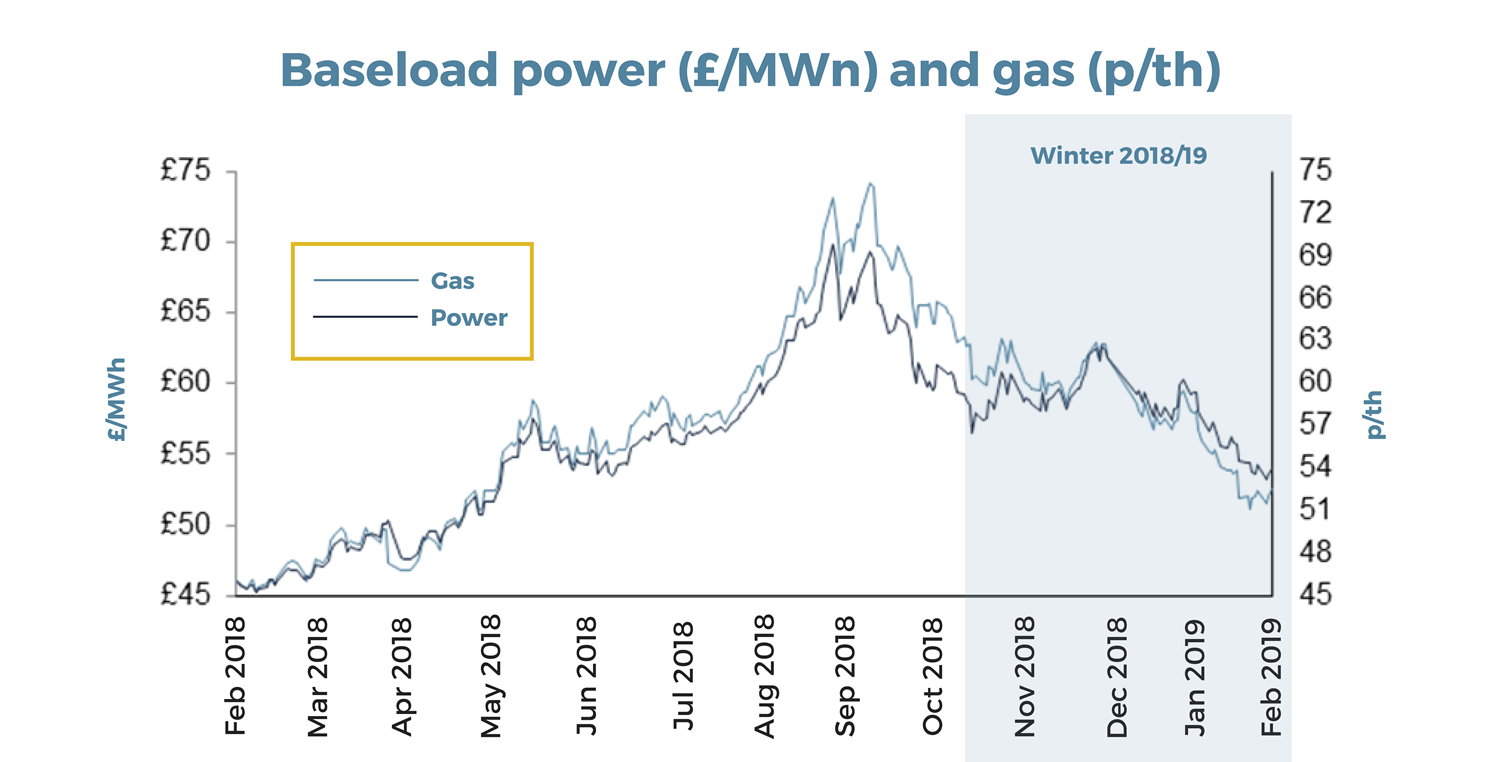

Following an extended spell of cold weather in February 2018 – which coincided with Britain’s first winter without Rough storage – gas prices peaked at near ten-year highs in September. This was largely due to demand for gas injections needed to restore the storage levels previously rinsed by the so-called ‘Beast from East’. At the same time, the oil market made a dramatic recovery last year, fuelled mainly by geopolitical factors, causing a corresponding spike in power prices.

Winter 2018/19 – What has caused wholesale costs to fall?

Gas

Between October 2018 and February 2019, the UK imported 57 cargoes of LNG, 43 more than the same period a year before. China’s high demand for LNG quickly fell after the summer heatwave ended, due to a warmer than forecasted winter. Meanwhile, a warmer winter in Europe limited demand for gas while previously depleted stockpiles were building back to full capacity. Norwegian gas fields also recovered from their maintenance period and began exporting at full capacity, further reducing demand for LNG.

Power

British nuclear stations also completed their maintenance season, further reducing demand for fuel-fired generation. Renewable wind generation, meanwhile, output an average of 7GWs in November, before falling to 6GWs in December. This was higher than the previous year’s output of 5GWs in both months, demonstrating that renewable generation in the UK is strengthening.

Oil

Oil prices fell by 37.65% from its peak of $86.29 at the start of October to its lowest point of $53.8 by the end of December. However, it has strengthened by 22% to $66.45 since its New Year lows. Oil prices originally fell due to high production output from the U.S and OPEC+ nations, combined with a global economic slowdown reducing demand.

Outlook – What is the forecast for energy costs in the future?

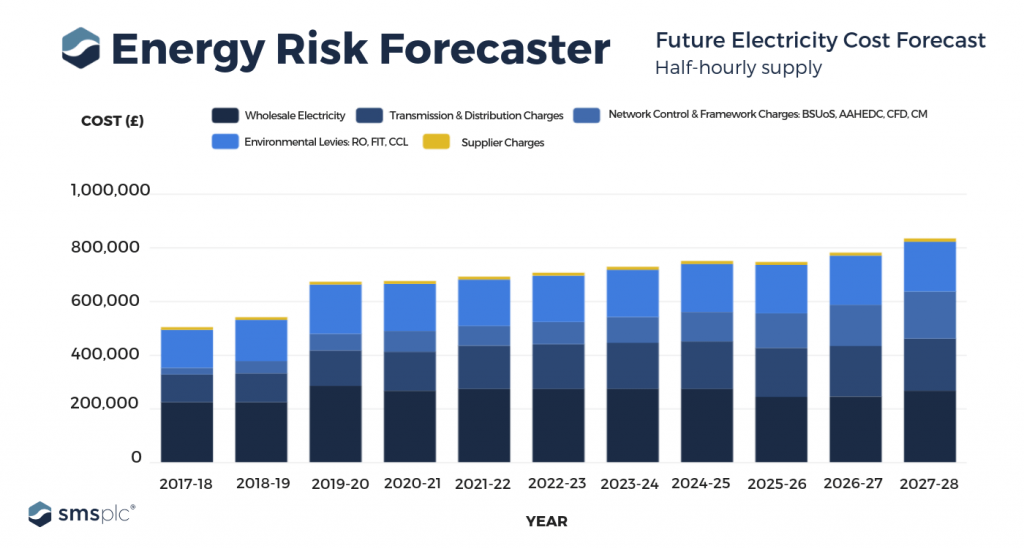

Although wholesale energy costs have fallen since the highs of last summer, with gas and power prices combined decreasing by approximately 15% since September 2018, risk remains high for energy consumers looking forward according to our market-leading, independently-verified Energy Risk Forecaster.

Though in the short term (throughout spring 2019) wholesale prices are expected to continue to fall, largely due to warmer than average temperatures capping demand and boosting renewable output, in the long term the outlook is certainly frostier for business energy bills.

Indeed, it is estimated that overall energy costs for UK business could increase by 55% by 2028 compared to 2017-18 prices.

With wholesale prices expected to remain volatile and comparatively higher than previous years (power costs over winter 2018/19 are up 18% compared to winter 2014/15) the major impact on business energy spend is set to come through the continued rise of non-commodity costs.

Alarmingly for businesses, a large share of forecast increases are expected to actually happen within the next two years, with overall energy prices estimated to rise 35% by 2020 compared to the past 12 months, largely due to the increase in the non-commodity elements of the bill.

Non-commodity costs – latest forecast

In our latest forecast, we have considered increases in the Contract for Difference levy and Renewable Obligation, both of which have rose above inflation rates during 2018, while also adjusting our figures for the Climate Change Levy (CCL). While the CCL was already set to increase 45% for electricity and 67% for gas in April 2019, the government’s decision to further increase taxation on gas in 2021/22 (rising to 60% of the value of electricity) is set to deepen the financial impact on large gas consumers in particular.

A significant increase in the costs related to changes to the Distribution Network Use Of System Charges (DUoS) have also been considered in updates to the Energy Risk Forecaster.

Meanwhile, though it was announced in December 2018 that the Feed-in-Tariff scheme will close on 31 March 2019, the government has proposed a replacement scheme for the export tariff called the Smart Export Guarantee (SEG), which is currently being consulted on. The government says this new mechanism should not have an impact on the amount of money that consumers pay for low carbon levies, and this is reflected by our forecast.

Our updated forecast emphasises a heightened sense of urgency for UK businesses to review their energy risk management strategies.

For instance, organisations are urged to reconsider their approach to energy purchasing, particularly given the current volatile context of the wholesale market and imminent rises in the Climate Change Levy as of April 2019.

Businesses are also strongly recommended to consider investment in other areas that affect their energy spend, such as billing and energy efficiency, in order to mitigate the longer-term financial impacts of energy price rises.

Businesses can get a clearer visualisation of this impact today by using SMS Plc’s updated and free-to-use Energy Risk Forecaster

About the Energy Risk Forecaster

The Energy Risk Forecaster provides a projection of your organisation’s annual energy costs until 2027-28. Simply choose the energy type (electricity or gas), enter your tariff and latest annual consumption rate, then let the Energy Risk Forecaster generate your results. Your estimated ten-year energy costs allow you to easily envisage the potential future financial impact on your business and can be used to inform an energy strategy that helps mitigate this risk.

The intention of the SMS Plc Energy Risk Forecaster is not merely to point out the direct price impact on businesses (and how this can be influenced by a smarter energy-buying strategy), but also call attention to the ripple effect of these extra costs on energy billing and consumption. In order to minimise risk of higher costs in coming years, organisations will need to take greater care over how they are invoiced for their energy (through comprehensive bill validation), and perhaps most pertinently, find ways to reduce the amount of energy they use through the implementation of monitoring, efficiency and flexibility solutions.

At SMS Plc, we are helping businesses look at the bigger picture of energy price rises, offering a holistic approach to energy risk management across procurement, billing, consumption and project delivery.

For a no-obligation discussion on the potential price impact for your business, and what steps you can take to mitigate this risk, get in touch. Call us on 02920 739535 or email us we’ll get back to you.